Small debts

Effectively managing debts, whether small amounts borrowed from friends or more substantial loans from banks, is crucial for maintaining financial health. The app provides flexible options to track and manage these debts, ensuring you stay on top of what you owe and what is owed to you.

Tracking Small Debts

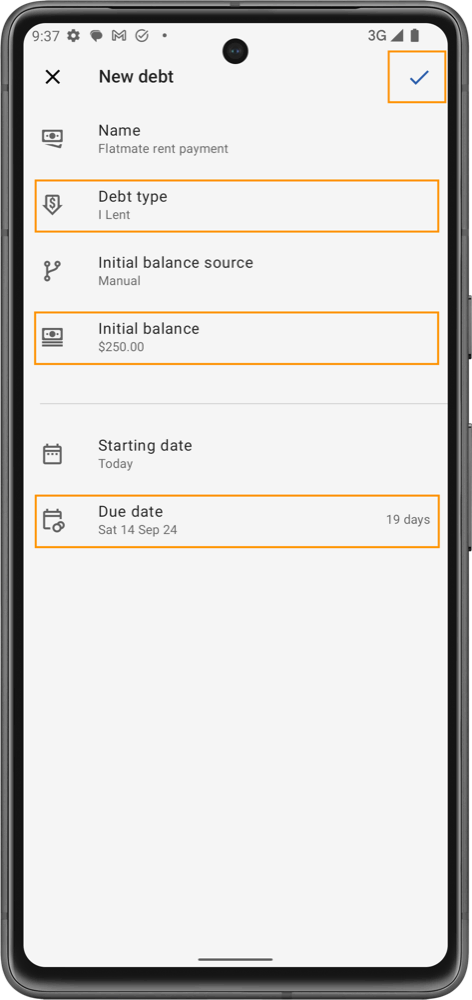

- Add a New Debt:

- Navigate to the 'New debt' option in the app.

- Fill in the debt details, including the name, type of debt (borrowed from someone, borrowed from a bank, or lent to someone), and the initial balance.

- Specify the starting and due dates for the debt.

- Manual vs. Linked Tracking:

- Manual Tracking: Enter the initial balance manually if you prefer not to link the debt to any specific transaction. This method allows you to adjust balances manually without affecting your overall budget.

- Linked Tracking: Link the debt to existing transactions in your budget:

- For money borrowed from someone, link to an income transaction.

- For money lent to someone, link to an expense transaction. This ensures that the debt reflects as part of your financial activity and impacts your budget accordingly.

- Bank Loans:

- For debts involving banks, such as car loans or mortgages, it's advisable to create a separate loan account. This account can then be used to track not only the principal amounts but also interest and any associated fees, providing a comprehensive view of your debt.

Adjusting Debt Balances

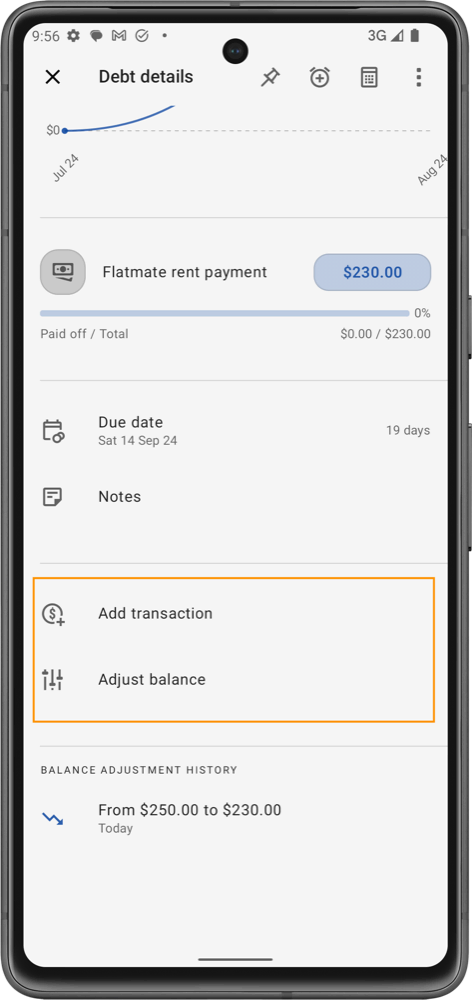

- Access Debt Details:

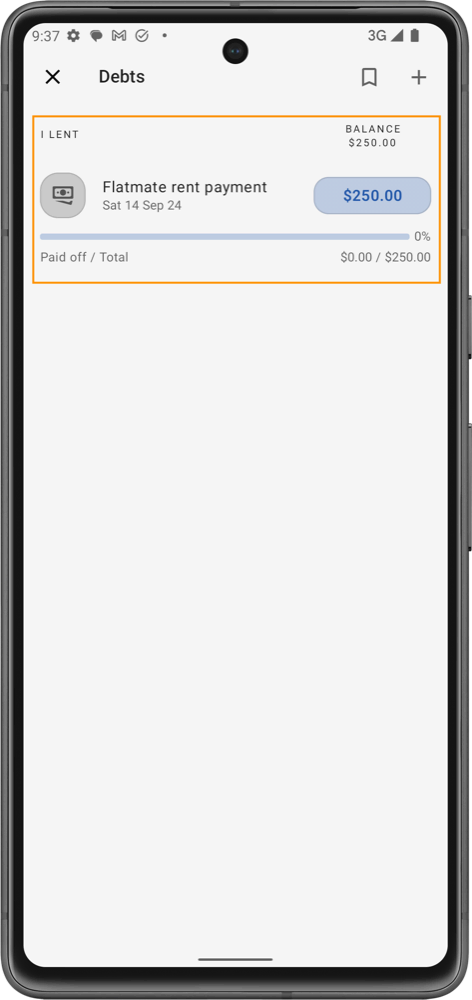

- Open the specific debt entry from your 'Debts' list to view detailed information and perform adjustments.

- Use the 'Adjust Balance' feature to update the debt balance manually. This is useful for recording payments towards the debt or adjustments if additional funds are borrowed or lent.

- Transaction Linking for Budget Impact:

- If you wish for the debt adjustments to impact your budget (reflecting payment or receipt of funds), create corresponding transactions within the budget:

- Add an expense transaction when making a payment on a debt you owe.

- Add an income transaction when receiving repayment on a debt owed to you.

- If you wish for the debt adjustments to impact your budget (reflecting payment or receipt of funds), create corresponding transactions within the budget:

Manual vs. Linking Transactions which to choose?

When managing debts in app, you have two primary methods to record and track these financial obligations: manual tracking and linking transactions. Each method plays a critical role depending on how you want the debt to reflect in your overall budget.

Manual Tracking

Manual tracking involves entering and adjusting debt balances directly without linking to specific transactions in your budget. This method is ideal for debts where you do not want the fluctuations to affect your current budget totals or when precise transaction details are not necessary for your financial tracking.

- Borrowing: When you manually track a borrowed amount, you enter the debt as a standalone item. Payments made towards this debt are also entered manually as adjustments to the debt balance.

- Lending: For money lent, you record the given amount as a debt owed to you. Repayments received are manually entered to adjust the balance of the debt.

Linking Transactions

Linking transactions to debts allows for a dynamic and integrated approach, where each debt is directly connected to specific financial activities in your budget. This method is suitable when you want to see the immediate budget impact of borrowed or lent money.

- Borrowing:

- Initial Transaction as Income: When you borrow money, the initial receipt of funds is recorded as an income transaction in your budget. This reflects the increase in your available funds.

- Payment as Expense: Payments made towards the debt are recorded as expense transactions. This directly reduces your budget's available funds, accurately reflecting your financial outflow as you pay off the debt.

- Lending:

- Initial Transaction as Expense: When you lend money, the amount given out is recorded as an expense transaction. This action decreases your available funds, showing the immediate financial impact of the money lent.

- Repayment as Income: As repayments are received, they are recorded as income transactions. This increases your available funds, reflecting the recovery of the lent amount.

Considerations for Choosing a Method

- Impact on Budget: Choose linking transactions if you want the debt to reflect immediately and accurately in your financial activity and budget calculations.

- Simplicity vs. Detail: Manual tracking is simpler and less detailed, suitable for informal or small-scale debts. Linking transactions provide a detailed record and are preferable for larger or more significant debts where tracking inflow and outflow is crucial.

In managing your debts you have the flexibility to combine manual adjustments and linked transactions. Even after a debt is initially created, you can manually adjust its balance and also link specific income or expense transactions to it. This hybrid approach allows you to maintain precise control over your debt records while ensuring your budget accurately reflects all financial activities related to the debt.

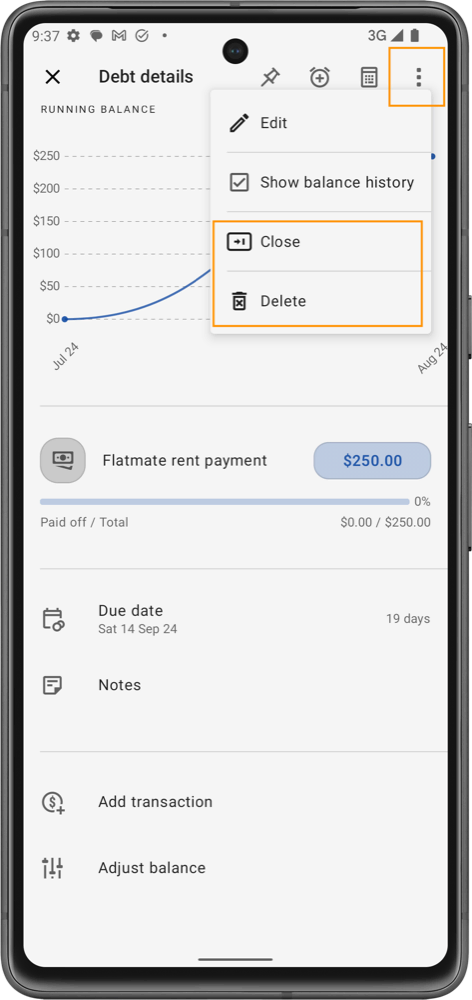

Closing or Deleting a Debt

Once a debt is fully paid off, or if you need to remove it for any reason, you can use the options within the debt details to either 'Close' or 'Delete' the debt. Closing a debt keeps its record within the app while stopping further tracking, whereas deleting it removes it entirely.

When you decide to close a debt, please note that this action is final. Once a debt is marked as closed, it cannot be reopened. Ensure all transactions and adjustments are complete before finalizing the closure of any debt.