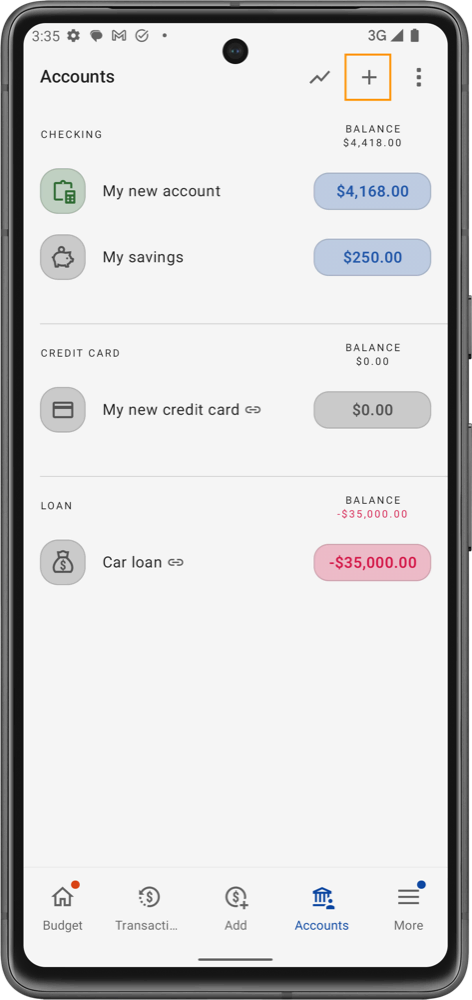

Large debts

Setting up and managing loan accounts in the app helps you track your debt while offering powerful tools to optimize your repayment strategy. Whether you're handling a mortgage, car loan, or student loan, the app’s debt calculator and goal-setting features make it easier to reduce interest and pay off your loan faster. Here’s a comprehensive guide on how to set up your loan accounts and take full advantage of these features.

Setting Up Your Loan Account

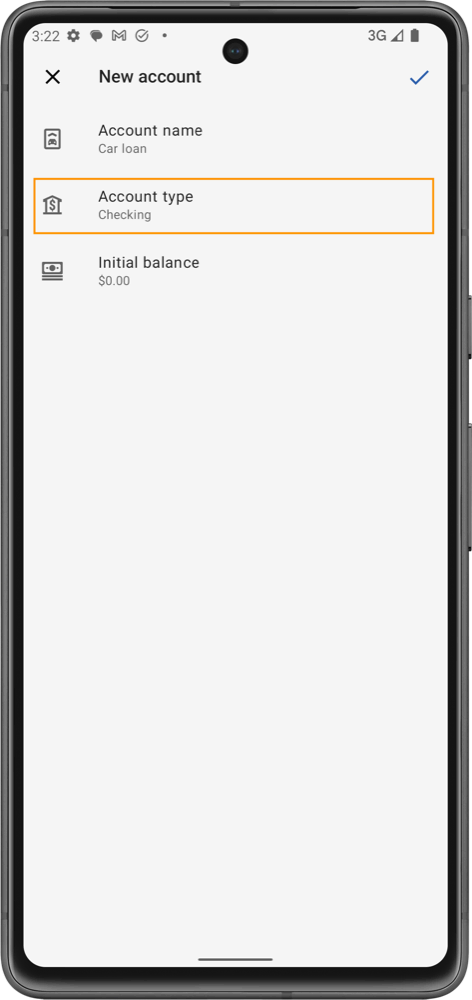

When setting up a loan account, you’ll need to fill in several key fields to ensure the app can track your progress and assist with repayment calculations. The setup process includes:

- Account Name: Give your loan a clear and descriptive name (e.g., "Car Loan" or "Mortgage").

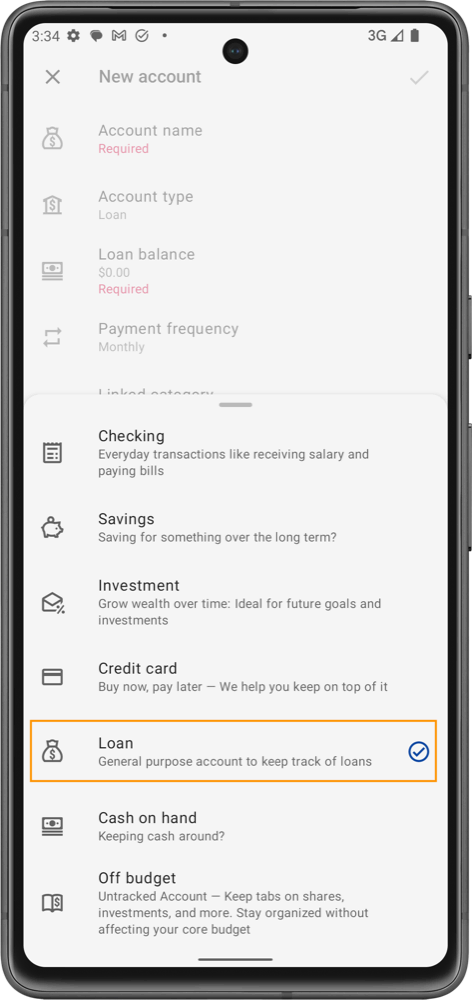

- Account Type: Select Loan as the account type. This differentiates the loan from other types of accounts like checking, savings, or credit card accounts.

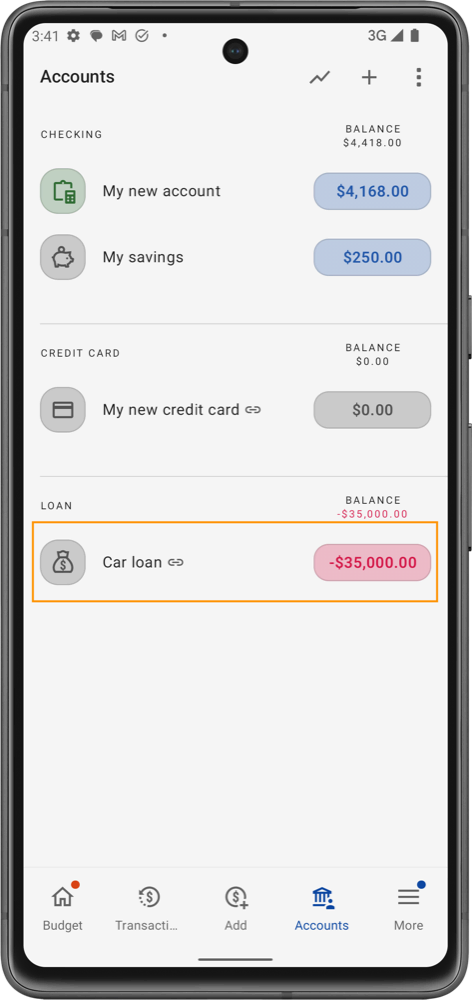

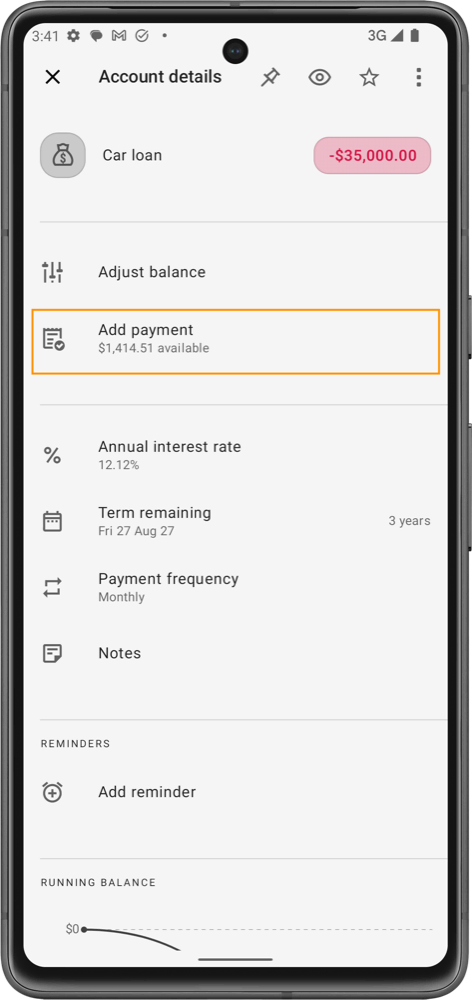

- Loan Balance: Enter the current outstanding balance of your loan (e.g., $35,000). This is the amount that you still owe and will be used to calculate your remaining debt.

- Payment Frequency: Specify how often you make payments, such as Monthly, Biweekly, or Weekly. This information ensures that the app can accurately track your payment schedule and calculate the term remaining.

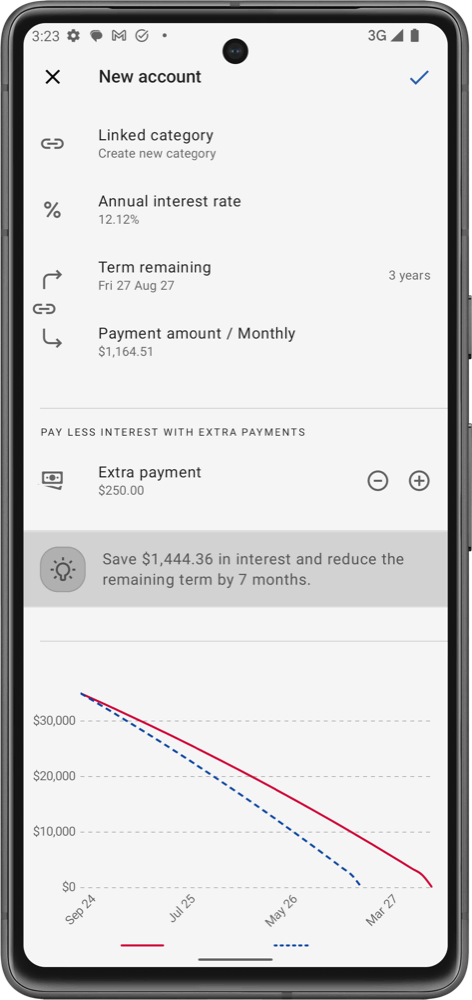

- Annual Interest Rate: Input the interest rate for the loan (e.g., 6.00%). This will help the app determine how much of your monthly payment goes toward interest versus the principal.

- Term Remaining: Indicate how many years or months are left on your loan. This is a compulsory field that helps you and the app calculate your exact payoff date based on your repayment plan.

- Payment Amount / Monthly: Input the fixed monthly payment or regular payment amount. This field is crucial as it allows the app to track your payments and ensure that the right amount is deducted from your budgeting category every month.

Advanced Loan Features: Debt Calculator & Repayment Goals

Once your loan account is set up, the app offers advanced tools to help you save money on interest and pay off your loan faster.

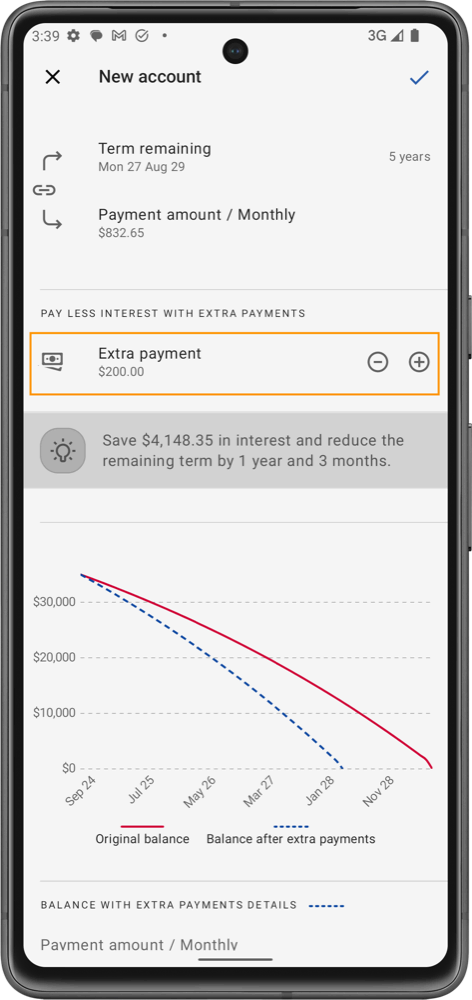

1. Debt Calculator: Reducing Interest and Loan Term

The debt calculator is a powerful feature that helps you explore how making extra payments can reduce the overall interest you’ll pay and shorten the life of your loan.

- Using the Debt Calculator: Once your loan account is set up, you can access the debt calculator. Input different amounts for extra payments, and the app will show you how these payments impact the remaining term and interest savings.

- Visualizing Your Savings: The debt calculator provides immediate feedback by displaying how much interest you’ll save and how many months or years you can shave off your loan term by making extra payments.

- Plan for the Future: By using this tool, you can strategize for occasional extra payments (such as using bonuses or tax refunds) to make a significant dent in your loan balance.

2. Setting Repayment as a Financial Goal

By fully utilizing the debt calculator and goal-setting features, you can strategically reduce your loan’s overall cost and eliminate your debt faster. These tools make debt management less stressful and more empowering, giving you a clear path toward a debt-free future.

Another key feature is the ability to set your loan repayment as a specific goal within the app, giving you a sense of progress and achievement as you move closer to becoming debt-free.

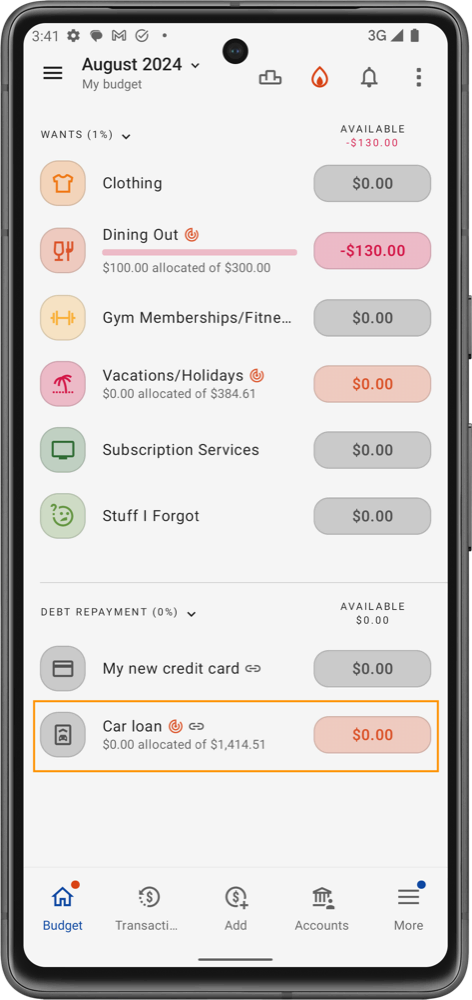

- Linked Category: When you set up a loan account, the app automatically creates a linked category for your payments (e.g., "Car Loan Payments"). This category is used to allocate the funds you’ve set aside for the loan.

- Goal Tracking: You can establish a repayment goal, which the app will track. For example, if you’re aiming to pay off your car loan within three years, the app will monitor your progress towards that goal and provide updates as you make payments. This keeps your financial plan focused and on track.

- Extra Payment Goals: You can also set up extra payment goals, which allow you to track one-time or occasional additional contributions, further accelerating your debt payoff.

Making Payments & Tracking Progress

You can also manually adjust the loan balance at any time without it affecting the rest of your budgeting. This feature is useful for making corrections or updates to your loan tracking without disrupting your overall financial plan.

Once your loan is set up, the process of making payments and tracking your progress becomes seamless:

- Allocate Funds to the Payment Category: Each month, ensure that you allocate the necessary funds to the loan payment category created during setup. This ensures that when it’s time to make the payment, the funds are ready and waiting.

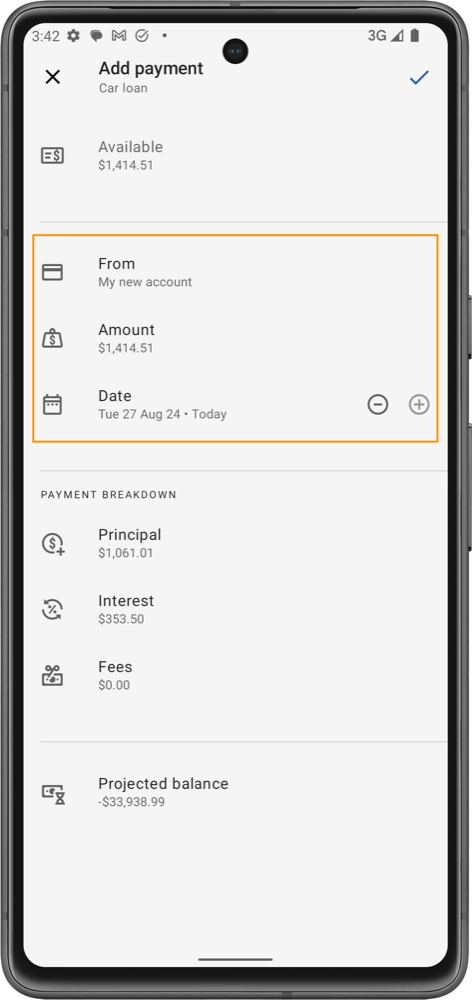

- Making a Payment: When you’re ready to pay, tap into your loan account. You’ll be able to add the payment details, including principal, interest, and any fees associated with that month’s payment. Once confirmed, the amount will be deducted from the linked loan payment category, keeping your budget in sync.

- Track Progress: After each payment, the app updates your loan balance, term remaining, and payment history. You’ll also see a progress graph that visually displays how your payments are reducing the overall balance.

Optimizing Repayment

The app is designed to help you get the most out of your loan repayments:

- Extra Payments: Use the debt calculator to plan extra payments, which can significantly reduce the amount of interest you’ll pay over the life of the loan and shorten the term. This feature gives you a clear advantage, as it allows you to see exactly how much time and money you can save with additional payments.

- Repayment Goals: Whether you’re setting a goal for your entire loan payoff or for specific extra payments, the app keeps you motivated by tracking your progress and helping you stay on course to financial freedom.