Credits & Refunds

Managing Returns

When handling credits or refunds the app offers flexible options based on whether you use Zero-Based Budgeting or Classic Budgeting. Refunds can either be treated as new income (if no category is selected) or revert spending within specific categories (if a category is chosen). Let’s explore how refunds work, their impact on your budget, and how they differ from actual income, like salary or wages.

Key Scenarios for Credits & Refunds

- Refund Without a Category (Income Ready for Allocation in Zero-Based Budgeting):

- When to Use: If no category is selected for a refund, the app interprets the amount as unallocated income.

- Zero-Based Budgeting Impact: The refund will appear as “Pending Allocation,” similar to regular income, and must be manually assigned to categories.

- Classic Budgeting Impact: In Classic Budgeting, the refund increases your overall account balance without requiring category-level adjustments.

- Example: You receive a $20 refund for a returned item and don’t assign it to a category. In Zero-Based Budgeting, this $20 becomes unallocated income that can be distributed across your budget categories. In Classic Budgeting, it simply boosts your account balance.

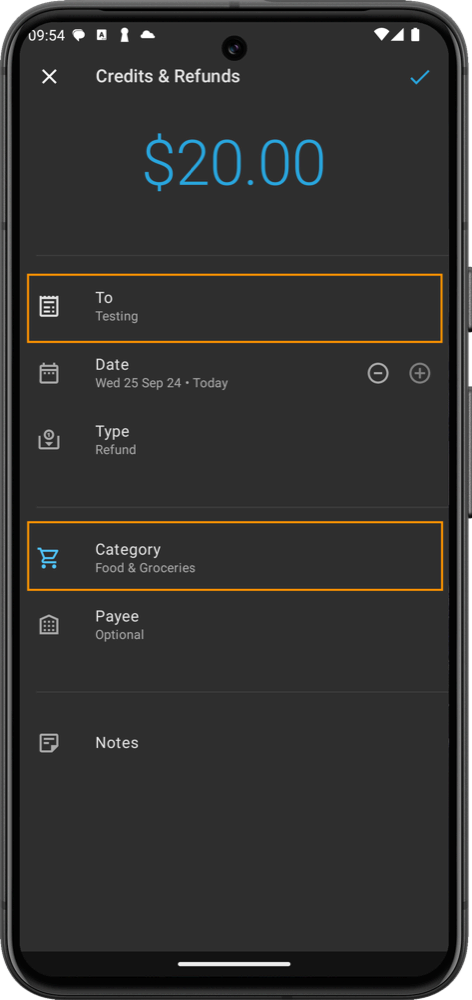

- Refund With a Category (Reverting the Expense in Both Budgeting Types):

- When to Use: If a category is selected for the refund, the app automatically credits the amount back to that category, restoring the balance.

- Impact in Both Budgeting Types: Whether using Zero-Based or Classic Budgeting, the refund is added back to the chosen category, effectively reversing the spending and allowing you to reuse those funds.

- Example: You receive a $30 refund for groceries. Assigning it to the “Groceries” category restores the $30 balance, making it available for future grocery spending.

Handling Cashback (credit) Rewards

You can choose whether to treat cashback as new income or to offset the spending in a specific category.

- Treating Cashback as Income:

- How it Works: If you receive cashback from a credit card or rewards program, you can treat it as unallocated income in the app.

- Zero-Based Budgeting Impact: The cashback amount will show up as “Pending Allocation,” similar to salary or other income. You can assign it to any category, including savings or other expenses.

- Classic Budgeting Impact: The cashback will increase your account balance, and no further action is needed unless you want to manually allocate it.

- Example: You receive $15 cashback on a credit card purchase and choose to treat it as income. This $15 becomes available for allocation in your budget, just like any other income.

- Offsetting a Category with Cashback:

- How it Works: Alternatively, you can choose to apply the cashback directly to the category related to the original spending.

- Impact in Both Budgeting Types: The cashback will be credited back to the selected category, reducing the overall amount spent in that category.

- Example: You spend $200 on groceries with your credit card and receive $10 cashback. You choose to apply the cashback to the “Groceries” category, reducing your total grocery expenses to $190. The app automatically updates the category balance to reflect the reduced expense.

How Refunds and Cashback Differ from Income

While refunds and cashback can increase your available funds, they differ from income such as salary or wages in important ways:

- Income is money earned from work or other sources, adding new funds to your overall budget. You must allocate it to your budget categories to manage expenses.

- Refunds and Cashback are not new income. Refunds return money previously spent, and cashback can either act as a reward to offset spending or be treated as additional income. They do not represent new earnings.

Example of Refund:

- You return a $50 item and receive a refund. If you assign it to the “Clothing” category, the $50 is restored to that category for future spending.

Example of Cashback:

- You receive $10 cashback on a credit card purchase and decide to apply it to the “Dining” category. This reduces your dining expenses by $10, adjusting your category balance accordingly.

Practical Use Case Examples

-

Scenario 1: Refund without Category:

You return an electronic item worth $50 and don’t select a category. In Zero-Based Budgeting, the refund will appear as unallocated income, requiring you to assign it to a category. In Classic Budgeting, it increases your account balance.

-

Scenario 2: Refund with Category:

You receive a $20 refund for a canceled subscription and assign it to the “Entertainment” category. In both budgeting types, the $20 is credited back to the “Entertainment” category, restoring the amount for future use.

-

Scenario 3: Cashback Applied to a Category:

After spending $200 on groceries, you receive $10 cashback. You apply the cashback to the “Groceries” category, reducing your total grocery expenses to $190.

-

Scenario 4: Cashback Treated as Income:

You earn $10 in cashback rewards from your credit card. Instead of applying it to a category, you choose to treat it as income. The $10 will be available for allocation to any budget category you choose — when using zero-based-budgeting version —.

Key Differences Summary:

- Income represents new money that you must allocate to your budget categories.

- Refunds restore previously spent money to either the account balance or a specific category.

- Cashback rewards give you the choice to either treat them as income or use them to offset specific spending in categories.

By understanding how to manage refunds and cashback, you can maximize their benefits and ensure your budget accurately reflects your financial reality.